It’s time to think outside the square for a win-win strategy

We have had numerous conversations with our business clients across the globe about the challenges they are currently facing. One common concern is the need to reduce the hours that their team members’ work as demand reduces, without compromising retention. That is, how do we negotiate reduced hours (sooner rather than later) and retain our people with a mind to having them return to regular hours once the world returns to a new normal and demand increases again. How do we look after our people and protect our investment in intellectual capital?

These entrepreneurs are struggling with their role (and in their words, their responsibility) to provide a living for their people and families AND to make sure that they remain financially sustainable in order to be in a position to re-employ in the future.

Here are 3 ideas we have come up with.

Idea No 1

We’re reducing our hours from 5 days a week to 4 days a week. We have asked our team to nominate a course that they would like to do to expand their professional knowledge or their skills or even a hobby they would like to pursue. We’re suggesting that they spend that day at home feeding their intelligence, positioning themselves to be even more valuable to the organisation, or learning a new skill which will allow them to do something they are really passionate about. We will assist them with the course costs and, if relevant, mentor them. In some cases, we will pay for course costs upfront. In other cases we will reimburse their education costs on their return to full-time employment.

Idea No 2

We’re reducing our hours from 5 days a week to 4 days. We have asked our team to nominate a charity that they would like to work with on that extra day at home. We’re helping them to decide how their current skills might be leveraged to the very best advantage. We’re discussing how we might help them to help others. We’re considering allowing them to accrue a day of special leave for each day spent volunteering. This special leave may be taken one day a month, 12 months after we have returned to full time employment – for example.

Idea No 3

We’re reducing our hours from 5 days a week to 4 days. We are partnering with other like-minded businesses to hire experts to educate our team around household budgeting, well-being and innovative thinking. It’s a shared investment in our people and it is delivered via video conferencing.

What do you think? Would any of these ideas work for you? What do you plan to do?

During times like this we need a sounding board, access to new ideas, conversations with innovative thought leaders, and to be able to tap into business acumen which speaks to the reality of doing business in difficult unpredictable times. Talk to us about how we can enable this for you – contact us now

We have heard talk of “building fences” around your clients, and introducing “another hook” – and it makes us shudder!

We ask you – what does this language say to you?

It suggests that the only way you can keep a client is to fence them in or hook them – and that is just crazy talk. This fear of losing a client and the underlying meaning around this language actually hooks into your subconscious and builds a fence around your thinking! It restricts your choices not that of your client.

The only way to ensure your clients don’t stray is to provide more value than your competitors do – you don’t need the hardware!

The best way to find out what clients value is to have “real” conversations with them – conversations that have transitioned from a transactional, reactive focus to one that is a relationship building, proactive initiative – a holistic future focused discussion.

Our CONVERSATIONS by DESIGN process addresses this and so much more.

If you would like to hear more about our CONVERSATIONS by DESIGN process, leave your details below:

* These fields are required.

Too often we ask for a sale before we have earned that right. Timing is everything – interact first – establish a relationship – articulate and agree the value – then ask for the sale. And here is a really simple, yet effective process to do just that.

Seth Godin tells the story of a guy (hence forth known as the Guy) in New York, back when old-school parking meters took quarters. The Guy asked Seth if he could give him a dollar for the 4 quarters he had. Seth did just that – handing over a dollar bill in exchange for the 4 quarters. The Guy then asked Seth if he could spare a quarter! Interesting approach??

So first, the Guy engaged Seth with a fair trade which may even have benefited Seth more because back then people were always looking for quarters for the parking meters. A relationship was formed.

Now the Guy knows Seth has a quarter (4 of them in fact). So his next request for a quarter is very hard to turn down. The Guy knows that Seth has 4 quarters and Seth knows that the Guy knows.

Compare this scenario to one where the Guy had just walked up to Seth and asked if he could spare a quarter. No engagement, no relationship – just a request for a “sale”.

Too often, we attempt to close a sale before we open it. Interact first, sell second.

How might this “story” play out in your business?

Let’s consider an advisory business.

You have reviewed the financial statements and noticed that there is a productivity issue – wages paid suggests available hours well in excess of hours billed – very easy to identify. You make recommendations which will increase charged and billed time or reduce wages costs – in either case there is a positive impact on the bottom line of the business of around $20,000. You have added significant value and your client acknowledges it – you have effectively opened the sale.

Now is the time to introduce the next opportunity – a service which will add even more value for our client for an investment of $5,000 – just one quarter of your clients increased profitability which was generated compliments of your advice. You have asked for the quarter!

How often do you add value with recommendations and then neglect to quantify or articulate that value to your client? What you think is obvious is not necessarily so, from your clients perspective.

When you make observations or recommendations, always articulate both the financial and non-financial benefits to the client and get buy in.

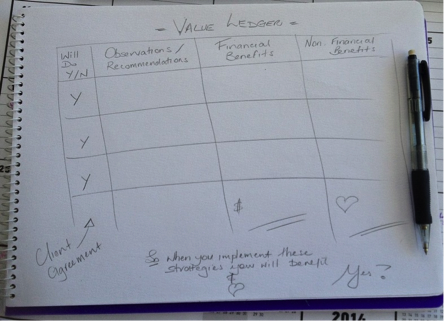

Try my “VALUE LEDGER”

1. As you progress through the meeting with your client, note down your recommendations and observations, along with the agreed value.

2. Then, towards the end of the meeting, summarize – go through the LEDGER and ask your client if they intend to implement the strategies and if they agree with the benefits.

3. Add up the financial benefits and write down the total amount.

4. You have established the value you have added and gained your client’s acknowledgement of the quantum of the benefit. You have made the previously invisible, visible.

Now you have earned the right to ask for the sale – to introduce your new proposal!

Very simple… and very effective.

PLUS: You have a reason to follow up the client – to see how they are going with their implementation process – the VALUE LEDGER becomes the basis for an Action Sheet and an accountability tool.

NOTE: Don’t be tempted to get a VALUE LEDGER printed up or to pre-fill it – it is much more effective prepared as you go, hand written, appearing impromptu – it becomes a jointly prepared document – owned by both parties.

TIP: Be prepared – Prior to the meeting, be clear on the recommendations you will make and consider the value that will be added and how you will articulate this and gain client agreement. And remember, as the meeting progresses there may be new recommendations, new observations – add these as you go.

WARNING: Don’t “give away” all the value in one sitting – be careful that you don’t go over the top in an attempt to prove your worth in order to earn your right. The new opportunities may be best included in your new proposal.

A DOUBLE WHAMMY: The advisors I work with in a broad range of industries, including the accounting, consulting, banking, law and financial planning sectors, have found that this process has created a double whammy of value.

1. FOR THE CLIENT > The VALUE LEDGER enables advisors to prove up the value they add – to leave their client in no doubt as to the benefits of doing business with them, AND

2. FOR THE ADVISOR > The process also establishes the value of the sale to the advisor and as a consequence, there is less resistance around pricing from the advisor’s perspective. The first sale must always be to yourself (before you make the sale to your client) – and a this a great way of establishing that the value exists – that price = value added.

My ADVISING by DESIGN and CONVERSATIONS by DESIGN products incorporate this and many other tools and insights – if you would like to know more please email us on connect@openinggates.com – We’d love to hear from you.

A case study, an insight and an opportunity to brainstorm with your team to be better advisors.

I have been working with advisors assisting their transition from a reactive transactional mindset to one that has a proactive, relationship building focus. It takes practice and awareness to balance knowing and focusing on the numbers, and wanting to talk about solutions, with the need to take the time to listen to the clients’ story – past, present and future – with genuine interest. It takes a learned skill to take a client on a conversational journey, that goes way beyond the transaction. It takes preparation to ask better questions so that you get better answers. It is so important to be able to read the energy in a room, to be very much aware of the intangibles.

Sometimes you simply need to slow down to speed up – in order to add even more value.

As part of my insight into what is really going on in interviews, I arrange to have “debrief” sessions post interview with the prospect and with the advisors.

The case study

Let me share one of my stories… A prospect (Ann) met with an advisor (Richard) (it was her first meeting, they had not met before) to discuss how he might help her get her business back on track. Ann had chosen Richard based on what she had read on his website and in particular because of the focus on business development advice. This initial appointment was arranged for 1 hour – because Ann had to be back at her business for a meeting.

I have 5 questions for both the advisor and the prospect –

1. To what extent did the meeting meet your expected outcomes?

2. To what extend did the meeting meet the outcomes of the prospect/advisor?

3. What did you learn about the Prospect/Advisor?

4. How well do did you connect with Prospect/Advisor on an emotional level?

5. What are the next steps?

So here is how it went…

1. To what extent did the meeting meet your expected outcomes?

Ann said her expectations where that Richard would give her some indication of how he might help her grow her business and return it to profitability. This didn’t happen and she was very disappointed. He didn’t really discuss any of the services she had read about on his website.

Richard’s outcome was to bring a new client into the firm and he thought he could place an 80% probability on a subsequent sale.

2. To what extent did the meeting meet the outcomes of the prospect/advisor?

Ann had no idea what Richard wanted to achieve and could only assume that he did meet his outcomes.

Richard thought Ann wanted to find a new advisor and he was pretty sure that she would want to do business with him, that she was impressed.

3. What did you learn about the Prospect/Advisor?

Ann appeared to have heard Richard’s entire life story, his previous jobs and why he changed career, his family situation, his hobbies and interests, his views on politics, he drove a Mercedes of some sort.

Richard learned that Ann owned a recruitment business and wasn’t happy with her current accountant. The business was located in the northern suburbs of Brisbane and she had employees (not sure how many). She drove a Jeep! Richard said he would have found out more if they had more time – the interview went for 1.5 hours.

4. How well did you connect with Prospect/Advisor on an emotional level?

Ann said that he was friendly but she felt confused and the meeting seemed to be all about Richard.

Richard said Ann wasn’t very forthcoming with information and seemed to be a bit closed.

5. What are the next steps?

Ann was not sure what the next steps would be – she thought he said he would be in touch. The meeting finished in a bit of a rush because it had gone over time and Ann needed to get to going.

Richard said he would send her brochures and ask her to send him some financial statements and other information he would need to prepare a proposal.

The Insight

Now you might think that this is an extreme example – let me assure you that it is not.

In most cases, what’s lacking, is preparation, an agenda and the recognition that it is the advisor’s role to lead the discussion. Winging it is a huge waste of everyone’s time and money.

Preparation begets opportunity. Every meeting must have an agenda – that is a well established strategy for a more effective meeting. Richard did not follow an agenda. But equally as important is the pre-start checklist – that is, what should be done in preparation for this meeting. A pre-start checklist and an agenda are non-negotiable. No checklist or no agenda – no meeting! It doesn’t matter how experienced you are.

Pre-start actions include:

1. Research your prospect

2. Research their industry

3. Identify the value you will add at this meeting

4. What is your desired outcome?

5. What are your “must knows”?

6. What are the key questions you must ask in order to take your prospect on a journey of discovery? Past, present, future.

7. What is your WHY – why do you do what you do?

8. How is your state – how are you being?

9. Meeting space on brand?

10. How will you meet the human needs?

11. Review the agenda

This is just a start and is not all inclusive. Creating a pre-start checklist is an important part of the process of building an advisory business and an advisors’ mindset.

The Brainstorm

Go back to Ann and Richard’s case study – what should have been done differently do you think? Work through this with your team. As you go through the process of brainstorming – develop your pre-start checklist.

And then be clear on when it must be used – my recommendation is, in every instance and for everyone – no exceptions.

Get started knowing that it will be an organic process – you will add more items as you go. And hold your own debriefs – what worked, what didn’t.

A Tip for the Agenda

The last item on your agenda should be BAMFAM – book a meeting from a meeting – when will the next point of contact be? Remember you are leading this process – be the instigator.

And your post meeting checklist

Another great opportunity to involve the team in innovative thought – what must happen post meeting?

If you are interested in developing your advisors to enable them to be even more effective, let us know – we would love to talk to you about our ADVISING by DESIGN process.